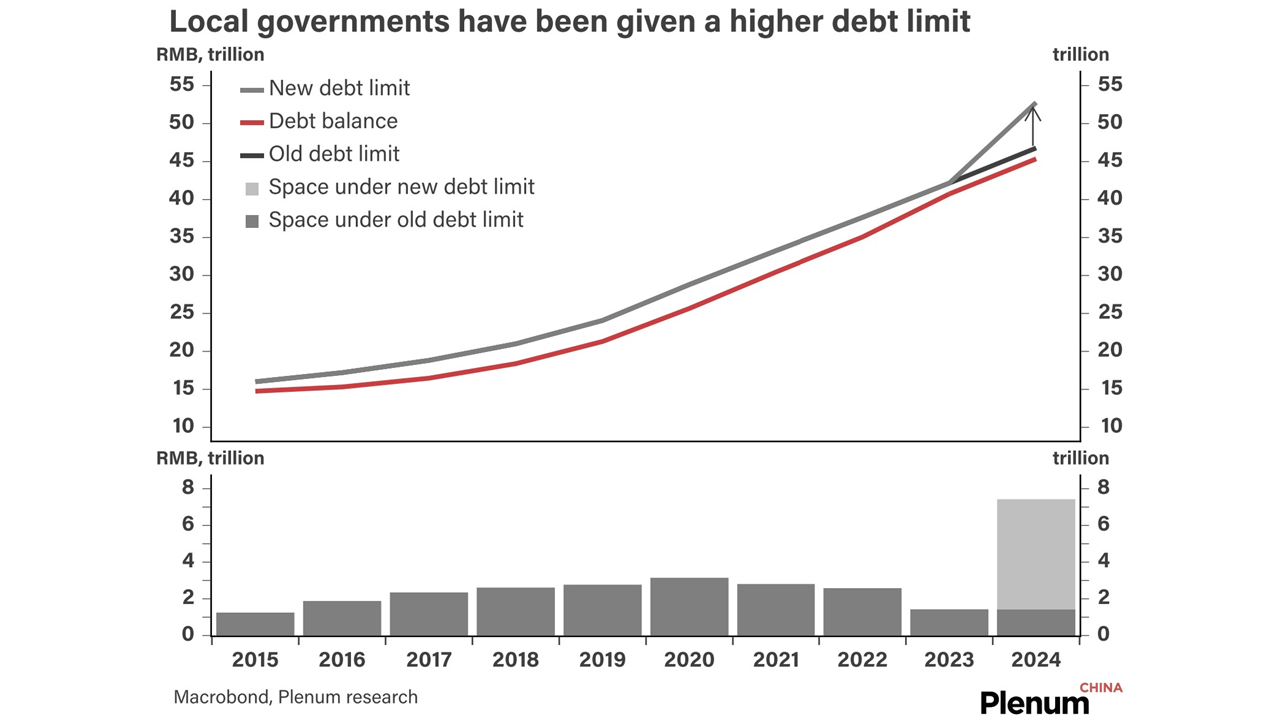

Beijing’s legislature has approved a RMB 10trn local government debt swap package that will last until 2028.

Beijing’s legislature has approved a RMB 10trn local government debt swap package that will last until 2028.

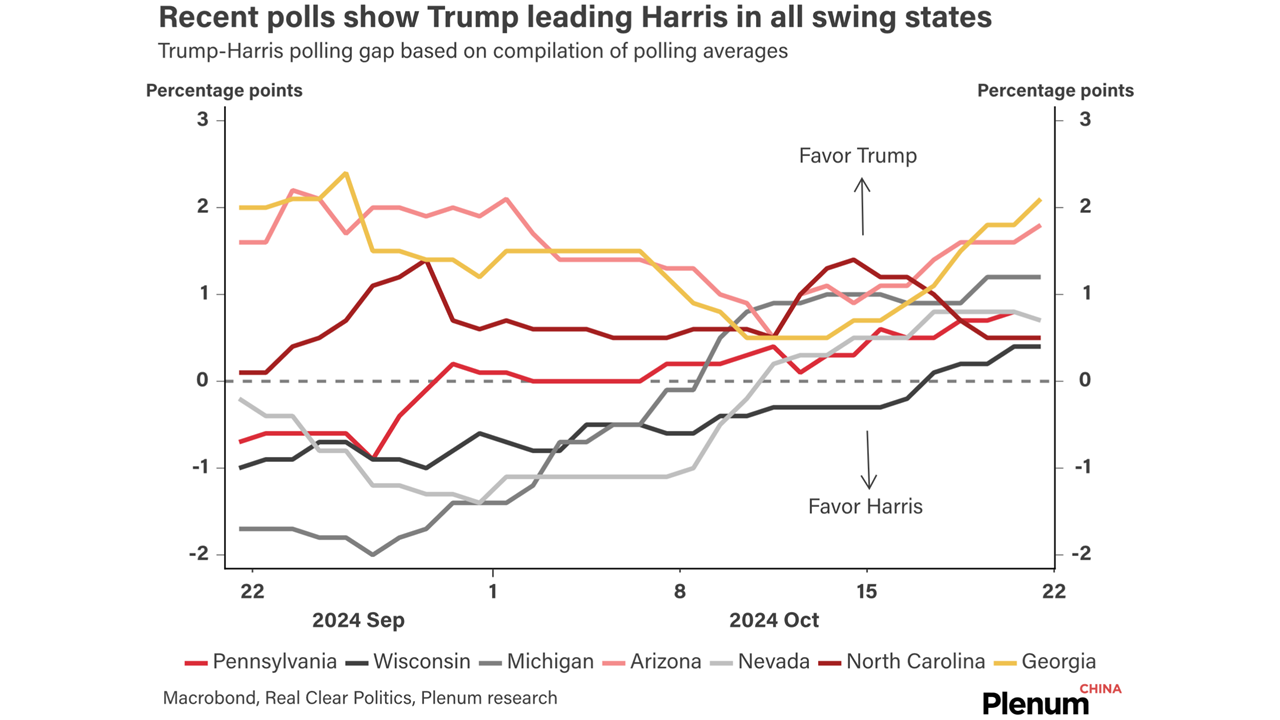

A quick take on Donald Trump’s victory in the US presidential election.

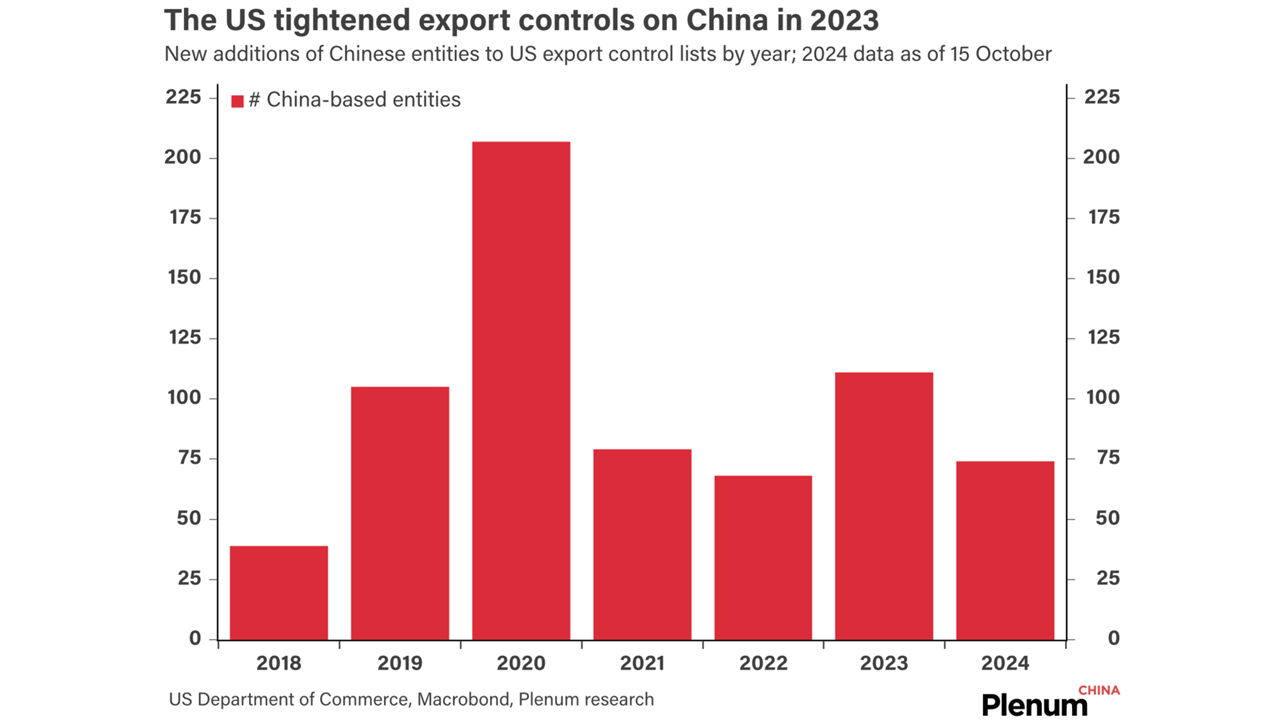

Technological decoupling from China will be one of the Biden administration’s most consequential legacies.

In this chartbook, we walk you through the latest developments in the Chinese economy and offer our outlook.

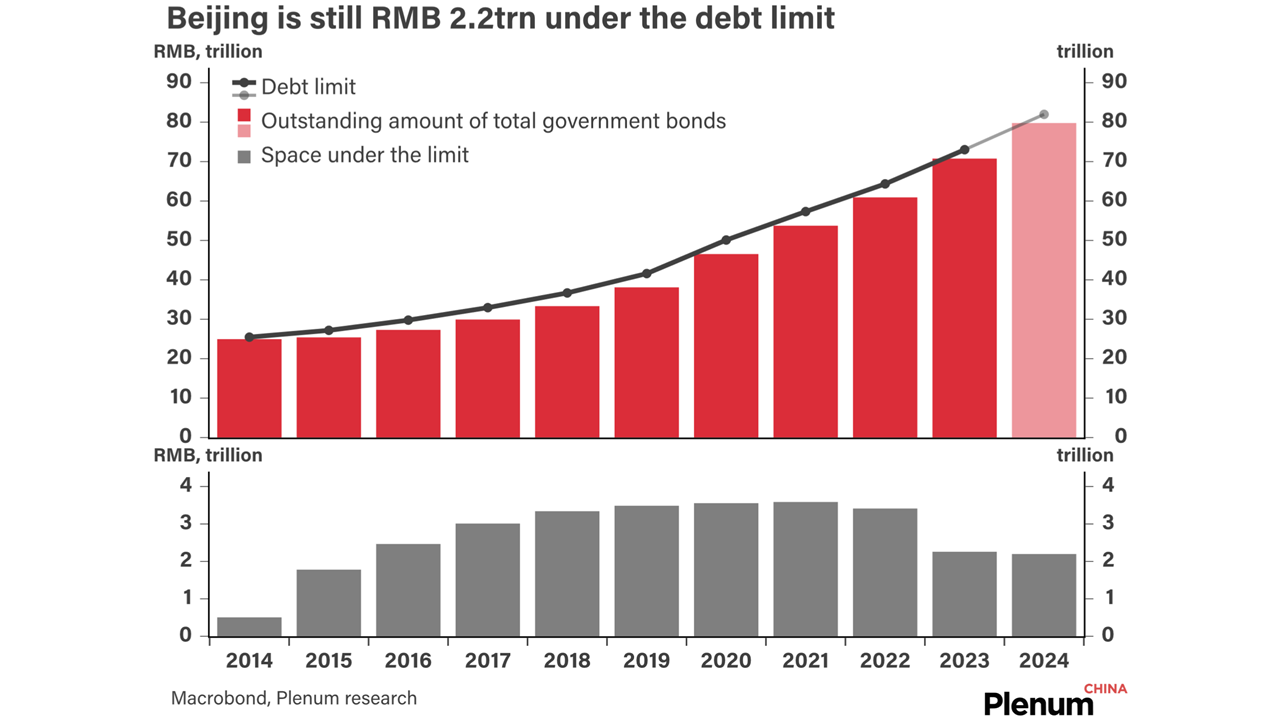

Beijing’s legislature is expected to approve a fiscal package at a meeting next week, which was scheduled later than expected.

The Republicans have the opportunity to take control over both the White House and Congress after the November election.

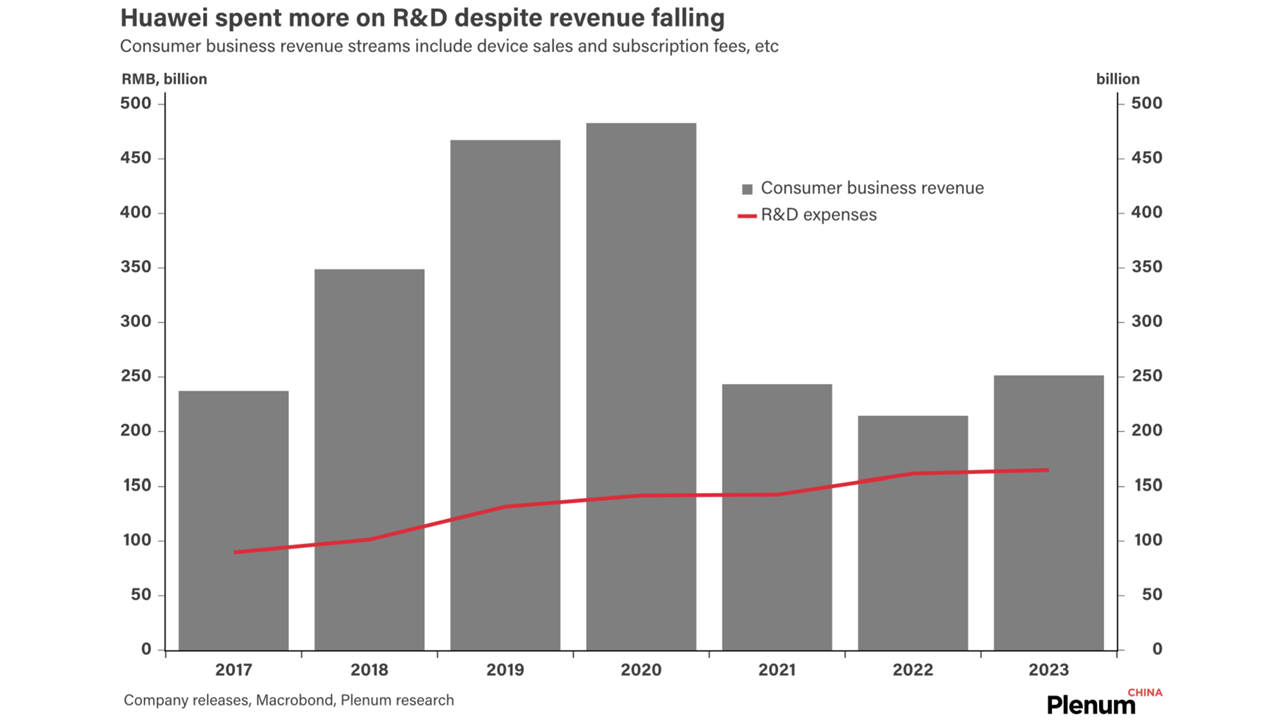

Huawei has developed a new mobile operating system for the mainland market that is completely separate from Android.

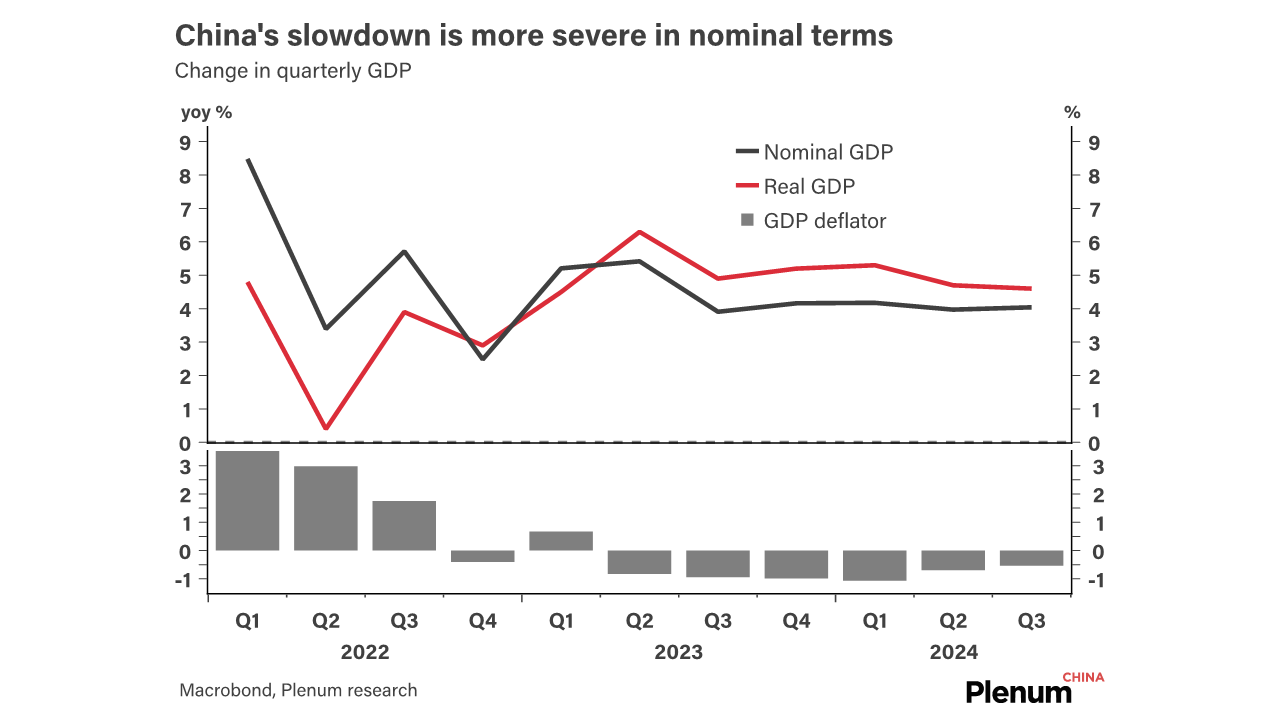

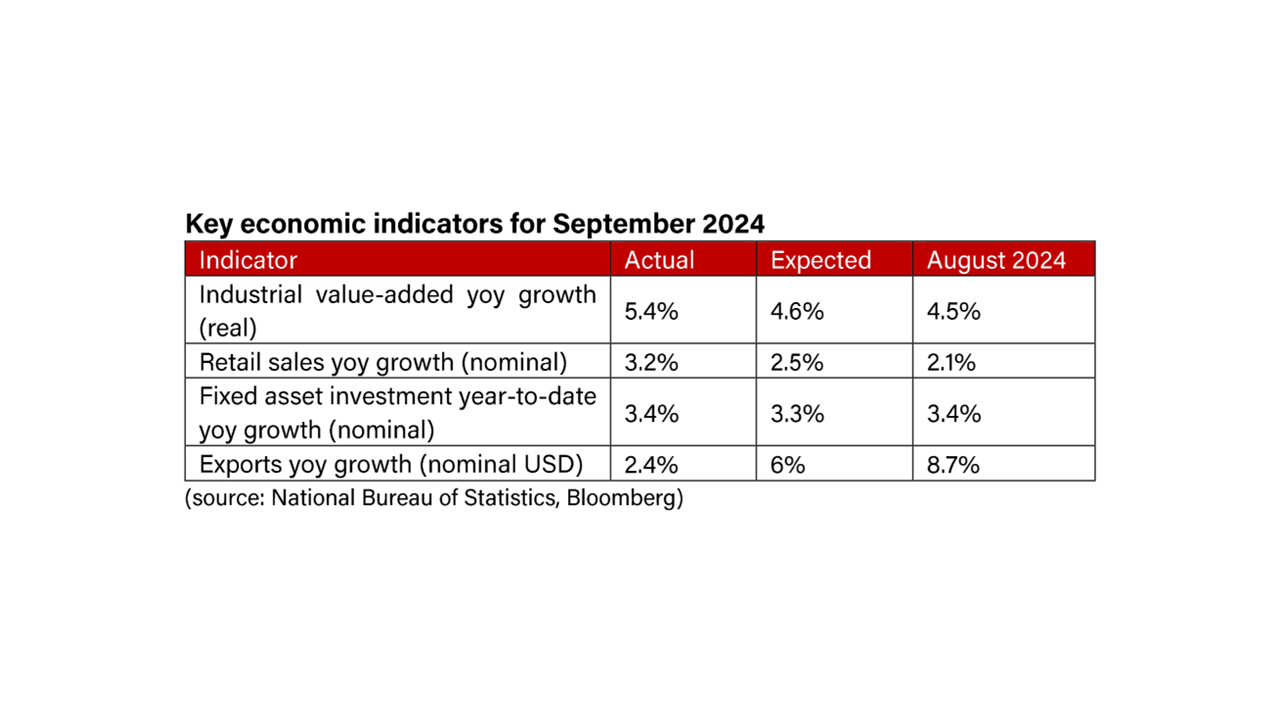

Domestic growth picked up slightly in September with the help of supportive policies, but export growth dipped.

The Ministry of Finance has committed to spending record money on derisking local government debt but has introduced little on boosting demand.

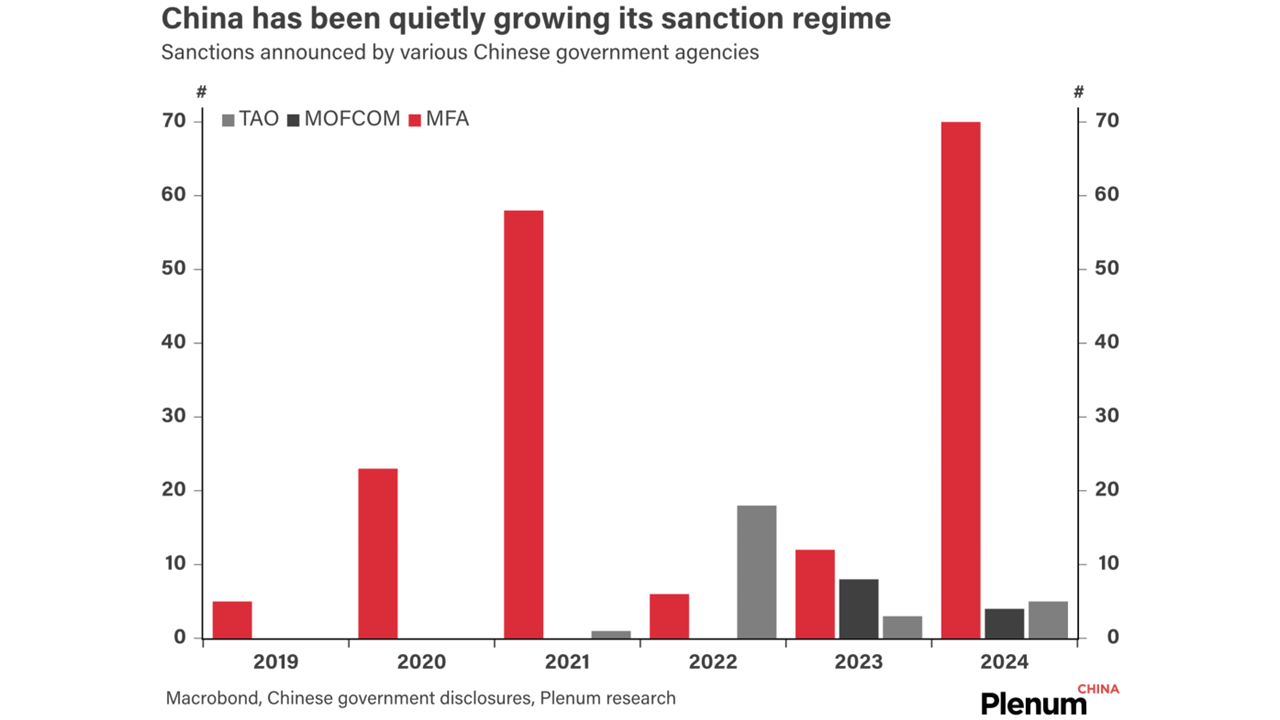

China has built up a sanction regime against foreign officials, foreign companies, and advocates of Taiwan independence.