Beijing released the major economic data for the first two months of 2020 this morning after the Federal Reserve cut rates to zero.

A global slowdown causes more troubles for Chinese exporters and forces Beijing to accept lower growth in 2020.

The PBOC seems more in line with the view that the COVID-19 is a supply-side shock and easing monetary policy can only help to a certain extent.

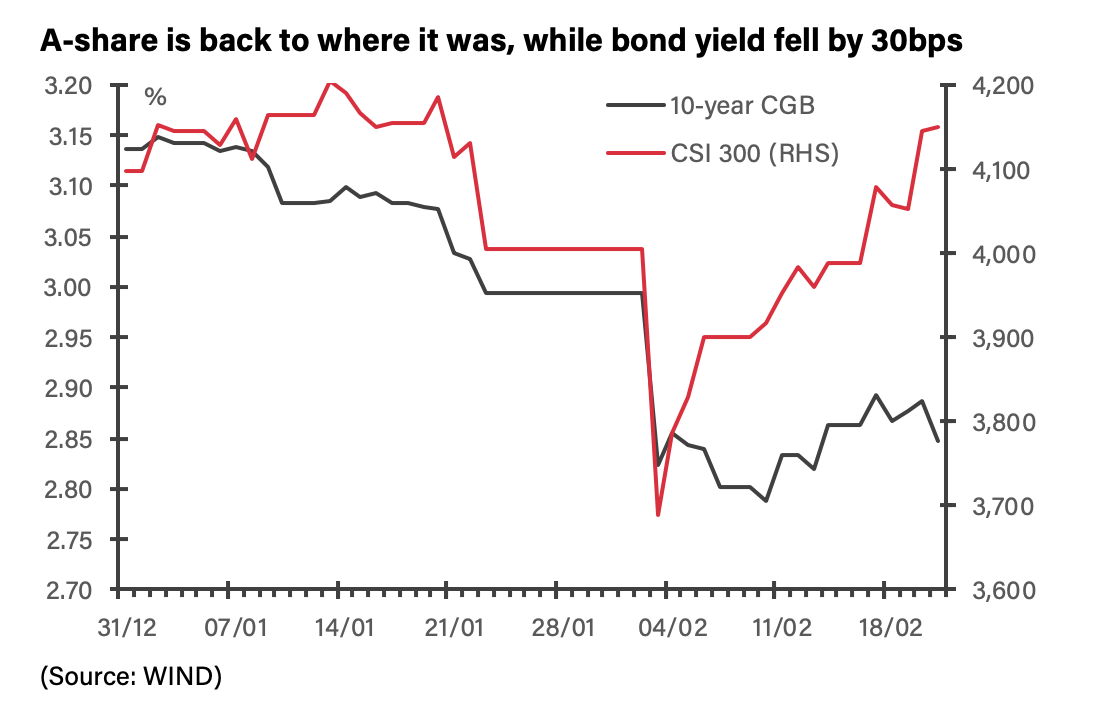

Chinese markets have seen remarkably different reactions to the COVID-19 outbreak over the past few weeks. The A-share market has fully recovered from the 12% sell-off in late January and early February. It has now rebounded back to where it was before the outbreak with the CSI 300 index up 1% year-to-date.

China’s current account surplus rebounded to $178bn in 2019 from $49bn in 2018, as both goods trade balance and service trade balance improved from last year. As a share of GDP, it rose to 1.2% from 0.4% in 2018. Most notably, outbound tourism spending fell to $255bn from $277bn. The surplus could rise further because outbound tourism spending can fall a lot more this year, and China’s import will slow down much more than export thanks to the outbreak.

Chinese government is putting more focus on restoring business operations, but the policy responses still fall short of expectations. The impact is going to be increasingly felt in the rest of Asia, and this time, countries will need to come up with their own measures to support the economy rather than waiting for Beijing to bail them out.