For Q4, growth was higher than expected in part because the National Bureau of Statistics slightly revised down the 2019 numbers.

2020 has been defined not only by COVID-19, but also by strategic planning for the next 15 years.

China’s fintech regulation seems to have taken a sharp turn following Ant Group’s delayed IPO.

The People’s Bank of China (PBOC) became the first major central bank issuing a central bank digital currency.

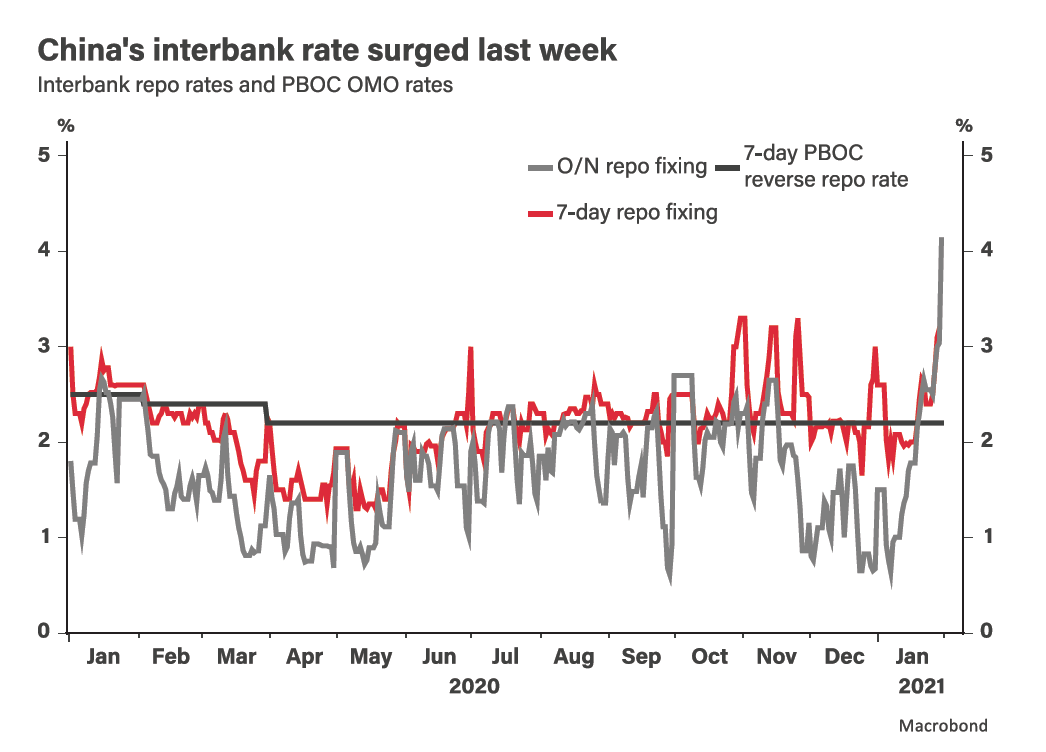

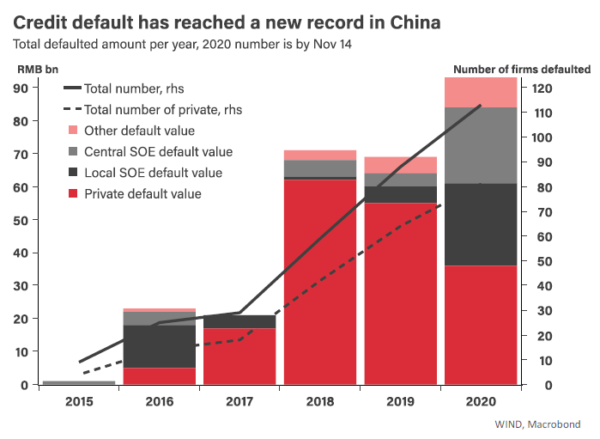

Beijing has urged local governments to be more proactive in dealing with local SOE defaults.

The latest credit market turmoil was triggered by defaults from local SOEs; this could cause a halt of bond issuance and slower credit growth