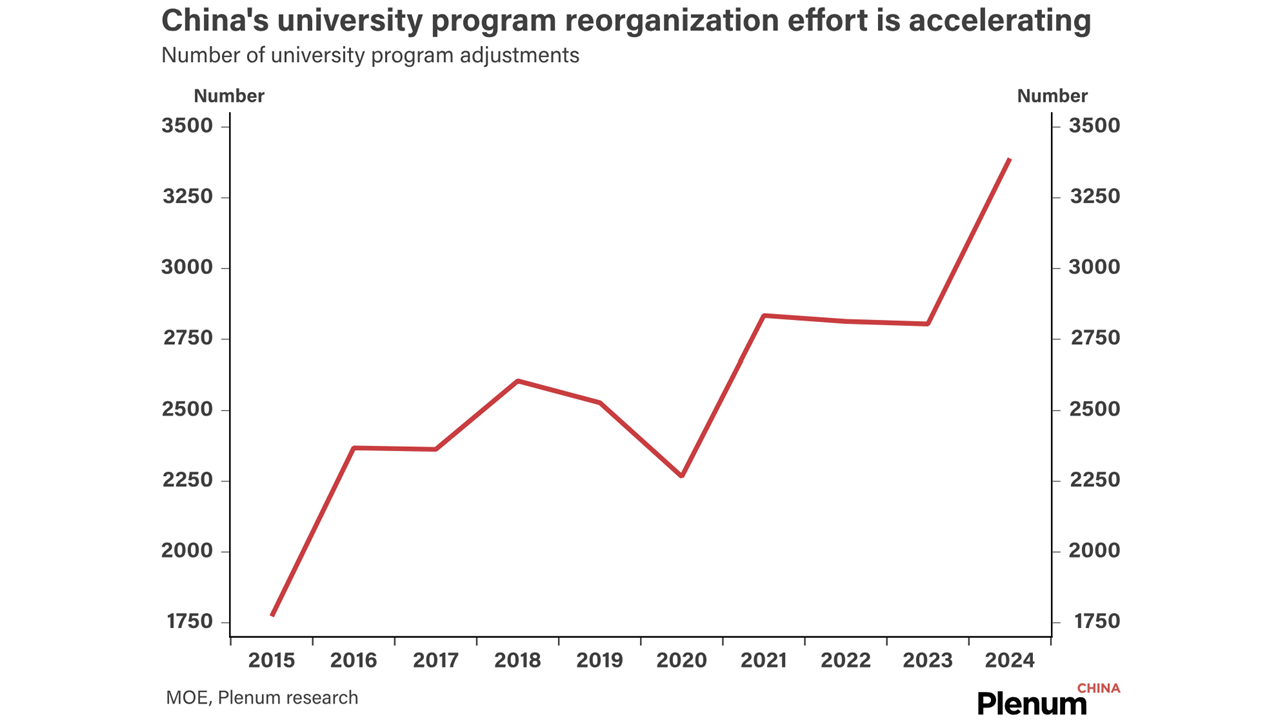

Beijing has accelerated its rebalancing of China’s university major offerings, limiting the growth of humanities majors and adding new engineering majors.

Beijing has accelerated its rebalancing of China’s university major offerings, limiting the growth of humanities majors and adding new engineering majors.

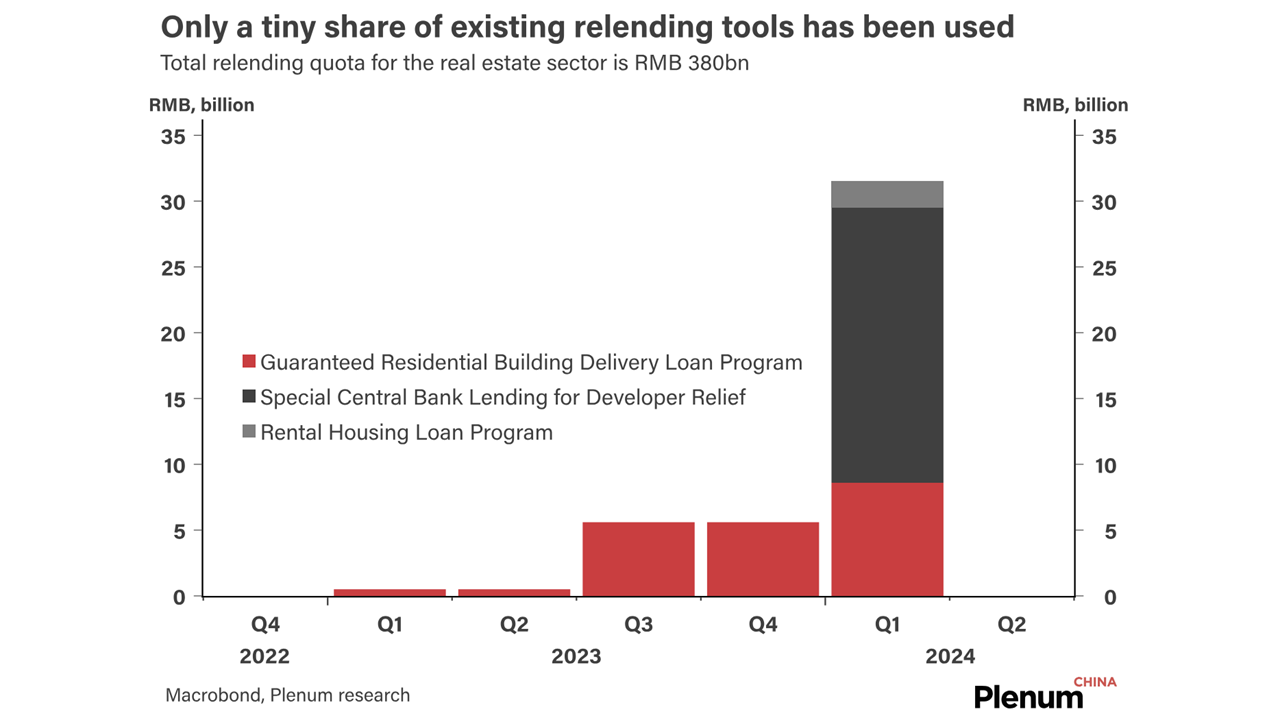

The central bank set up a RMB 300bn new relending tool to encourage banks to lend to local SOEs to buy up unsold housing inventory.

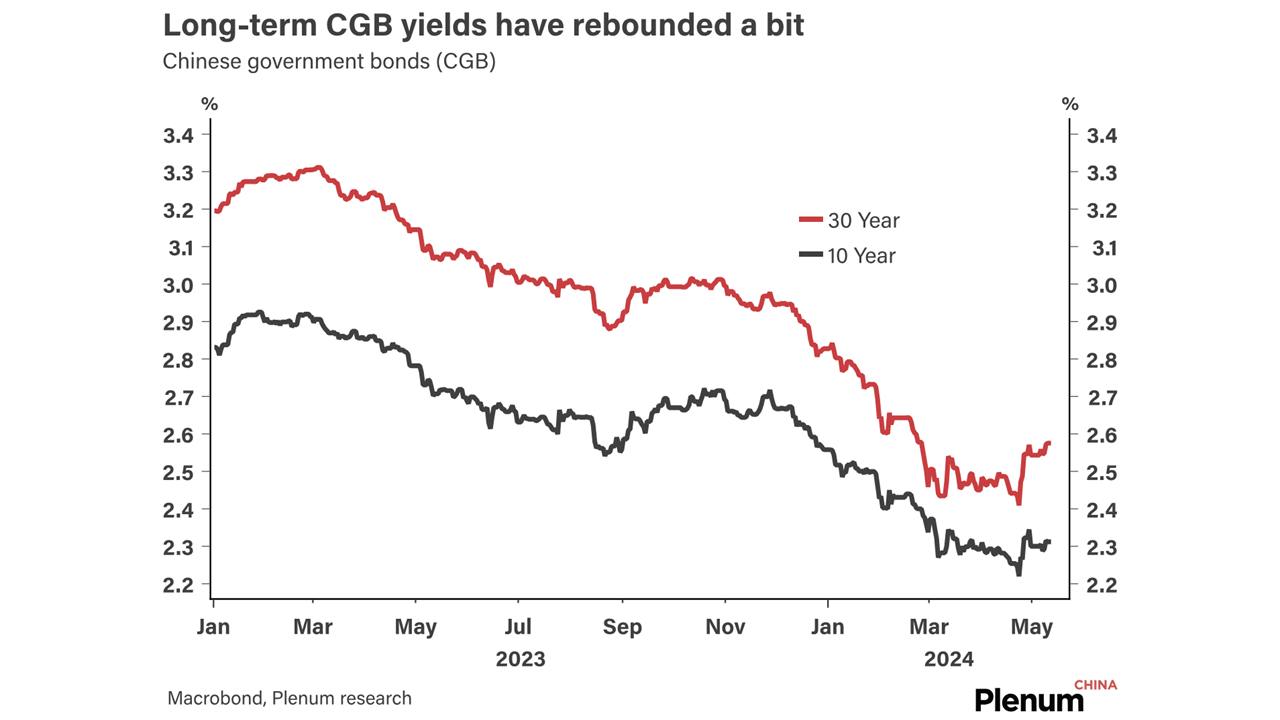

Long-term Chinese government bond yields have bounced back from the bottom after the central bank voiced its concern last month.

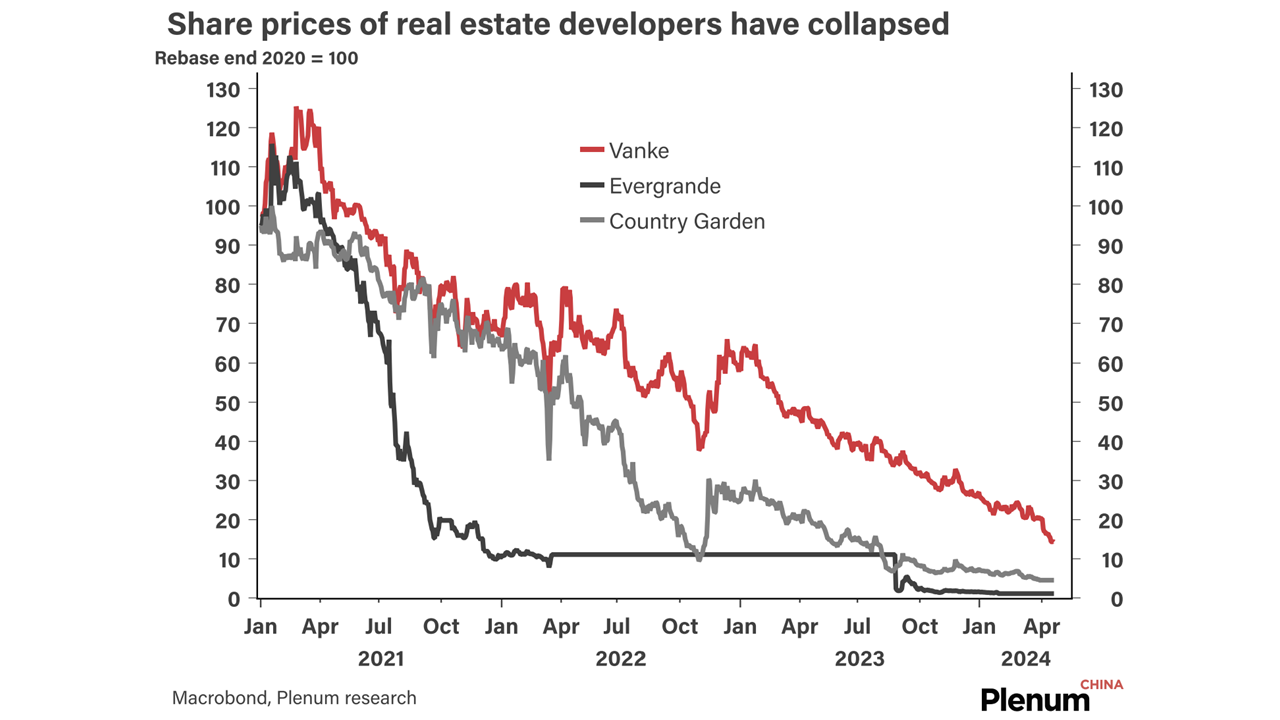

Politburo leaders are content with China’s economic growth but have endorsed more policy support for the ailing real estate sector.

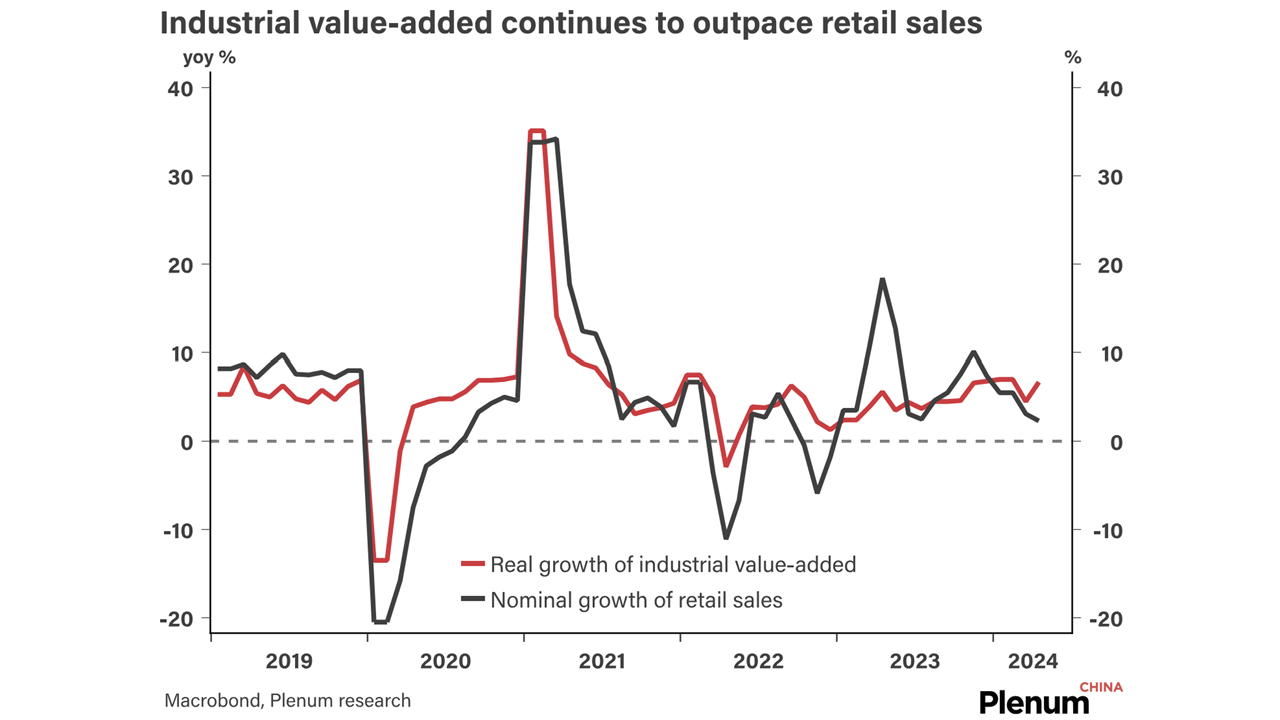

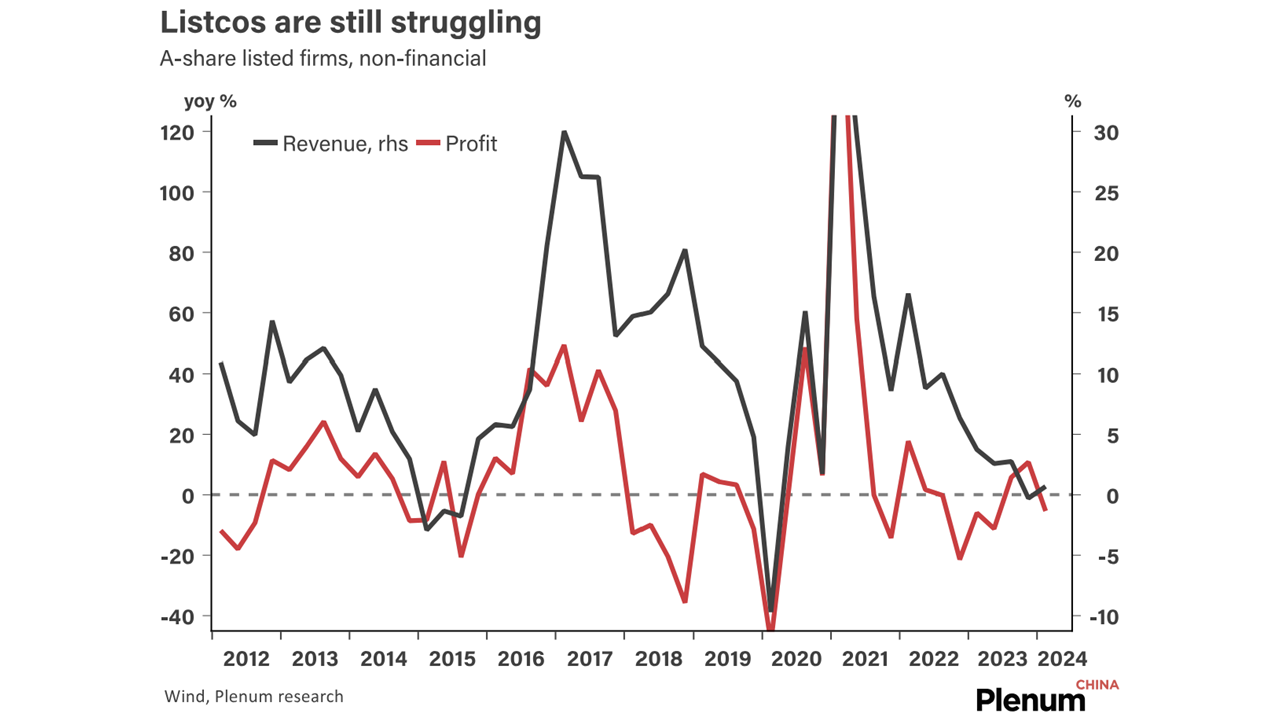

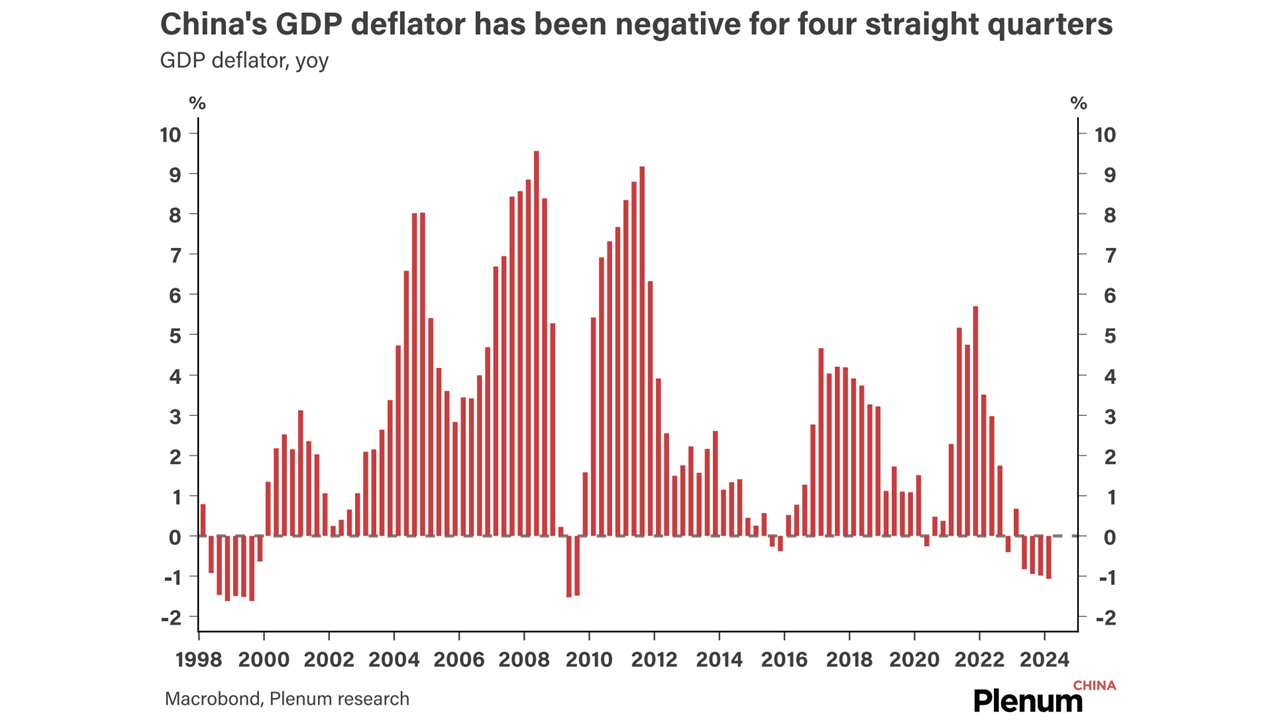

In this chartbook, we walk you through the latest developments in the Chinese economy and offer our outlook.

Beijing’s overall approach has been very hands-off; it has neither offered to rescue developers in trouble nor shut down the insolvent ones.

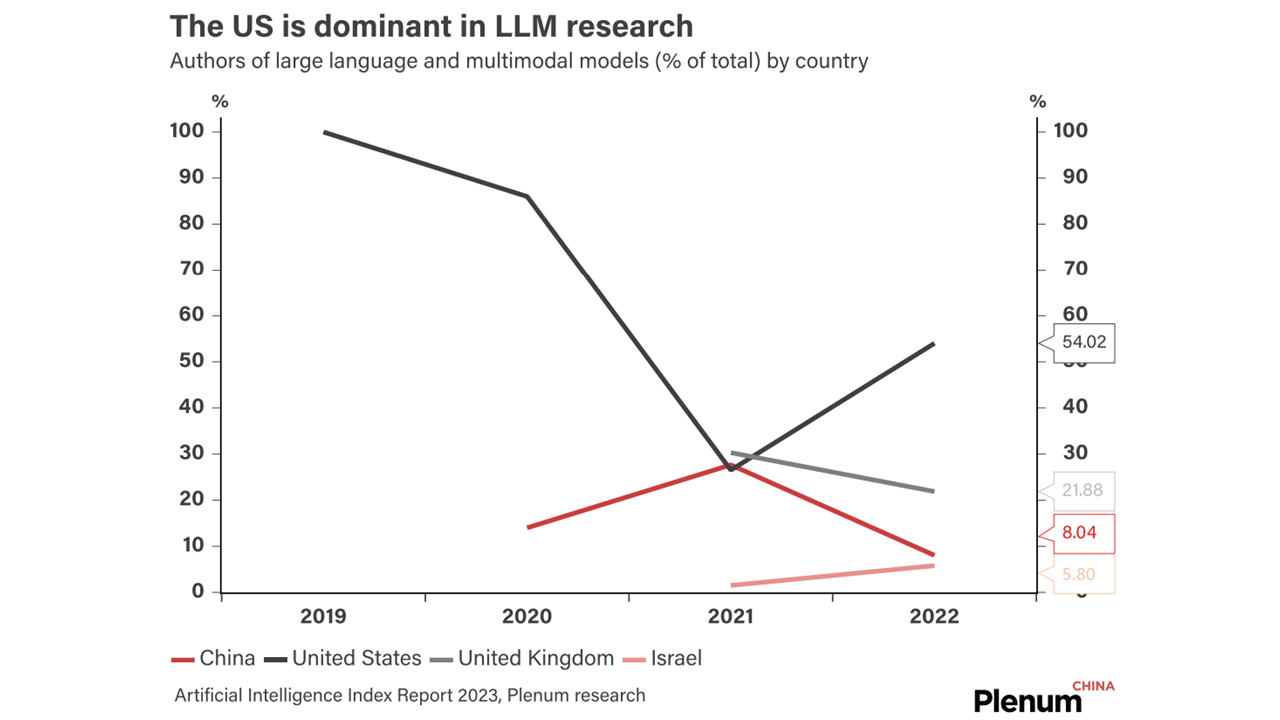

Despite moving early to control generative AI, China has been highly proactive in releasing policies to encourage the growth of the industry.