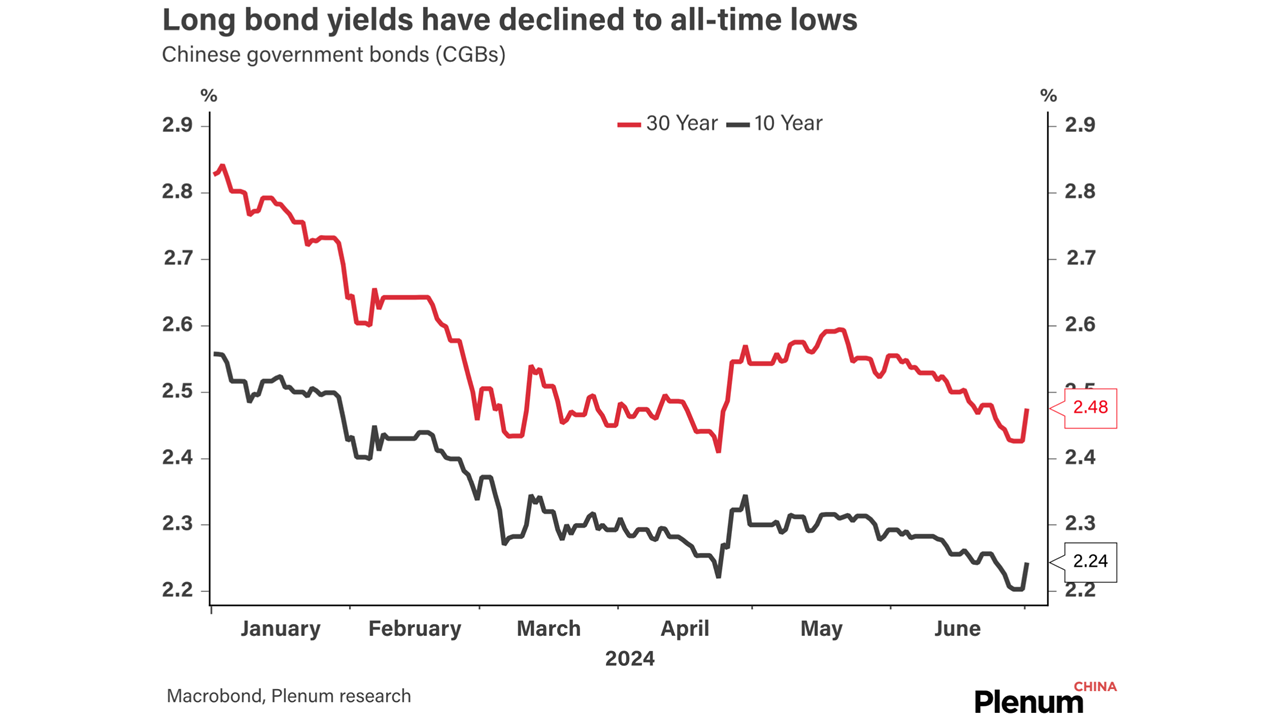

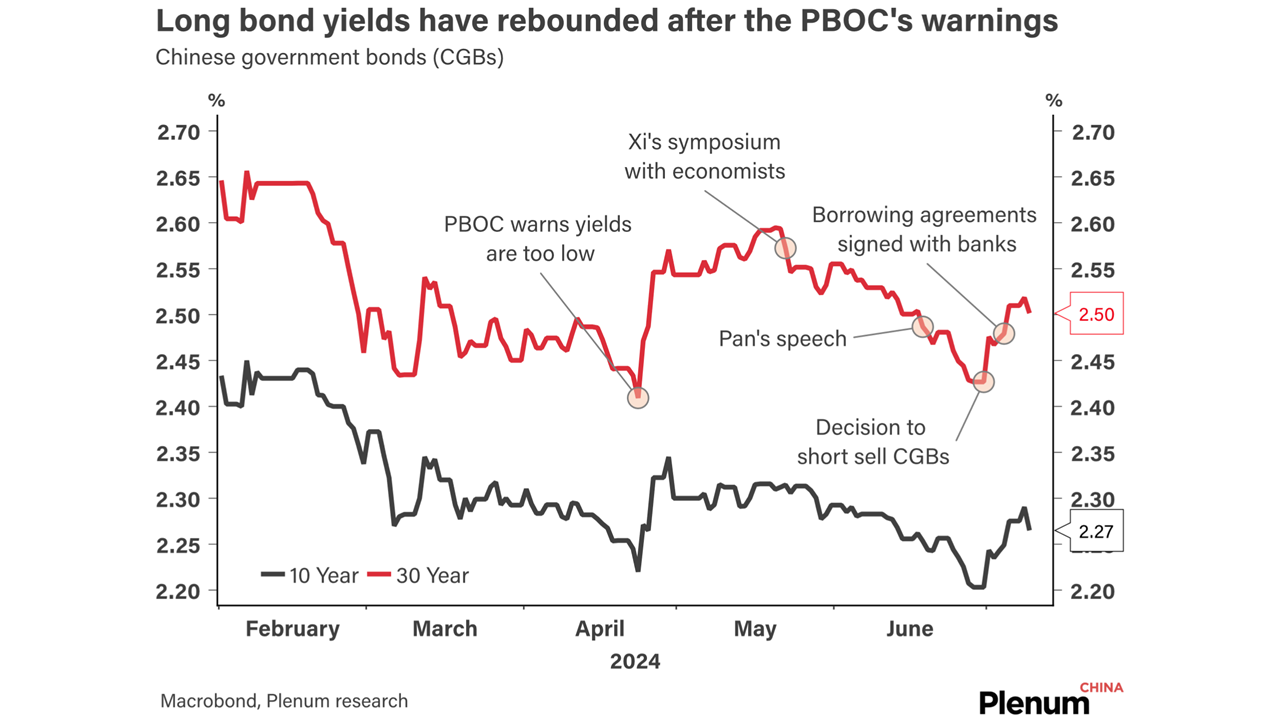

The PBOC has laid out more details on its plan to short sell government bonds; the measures will tighten liquidity in the interbank market.

The PBOC has laid out more details on its plan to short sell government bonds; the measures will tighten liquidity in the interbank market.

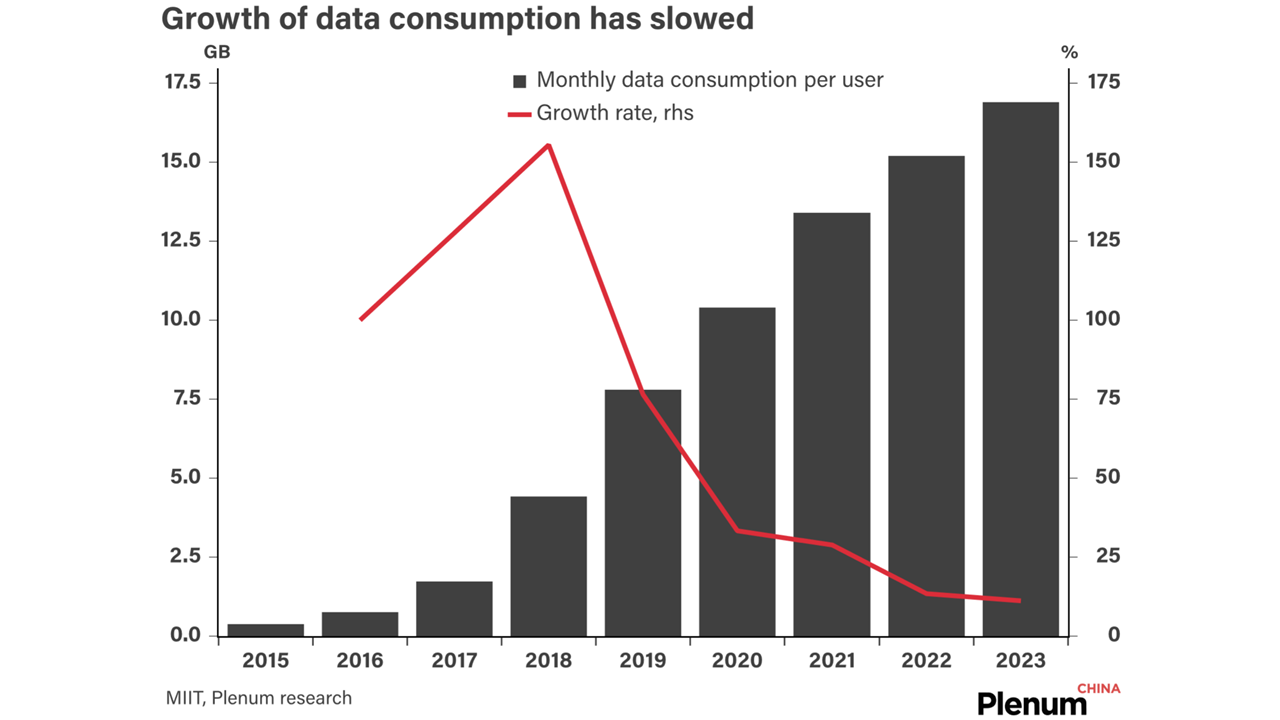

China moved quickly to build a nationwide 5G network and became a global frontrunner; now, local telecoms are scaling back their investments.

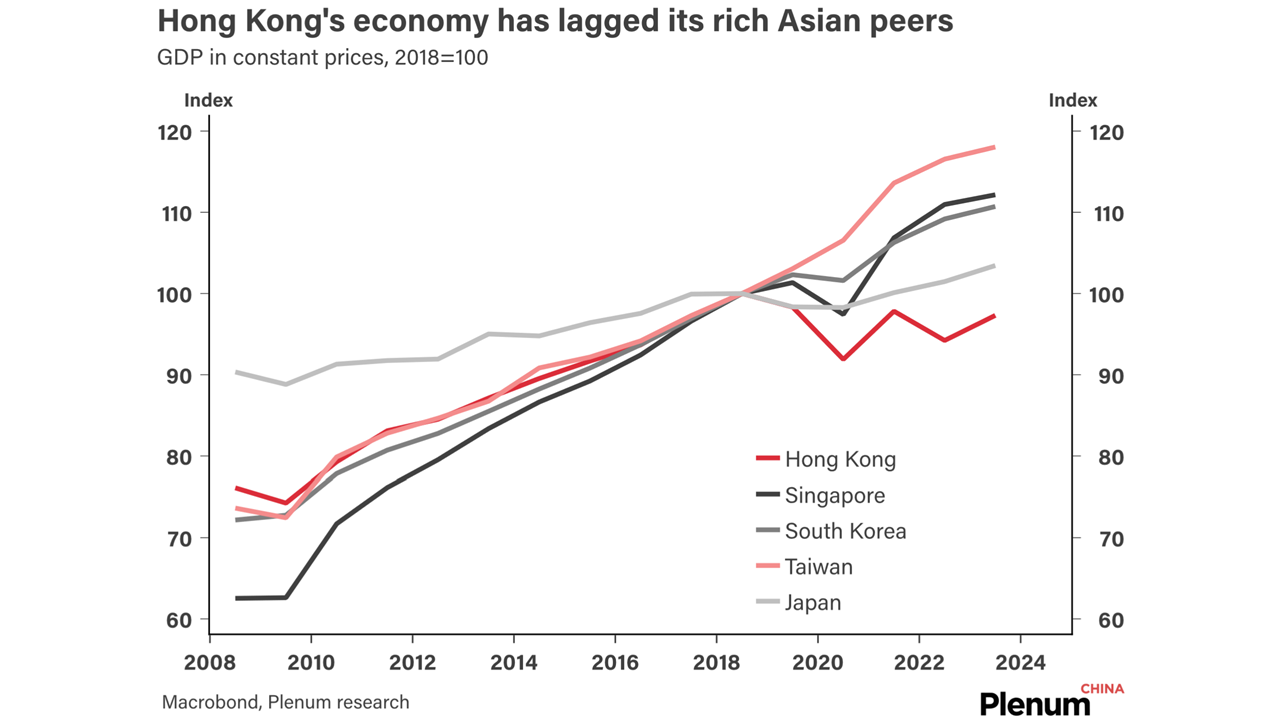

Hong Kong’s economy has been sputtering since before Covid, and it has lagged other developed economies in the region.

The PBOC governor defended the central bank’s monetary policy stance and implied that credit growth will not accelerate very much.

Retail sales improved in May, but most other areas slowed, including industrial production, real estate, and FAI.

Plenum clients are overwhelmingly interested in China’s housing market and the implications of a potential second Trump term.

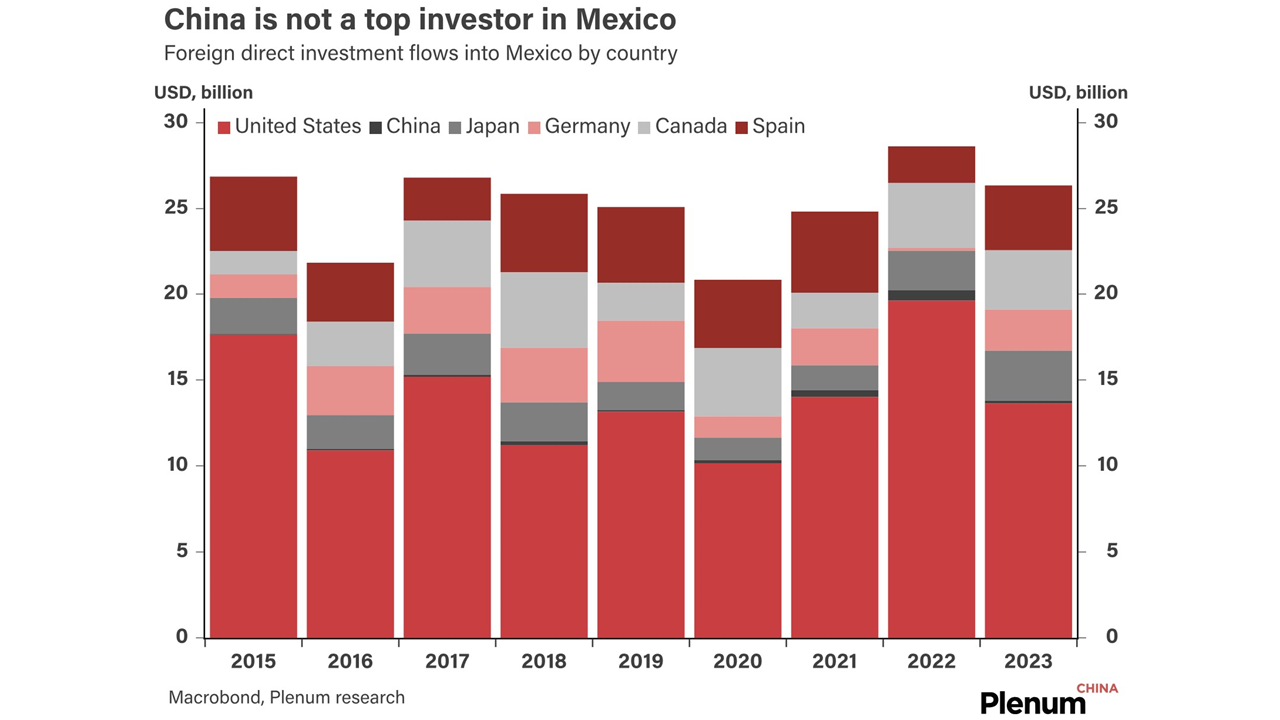

Chinese investment in Mexico has been growing rapidly, but it still remains relatively small compared to the investments made by other countries.

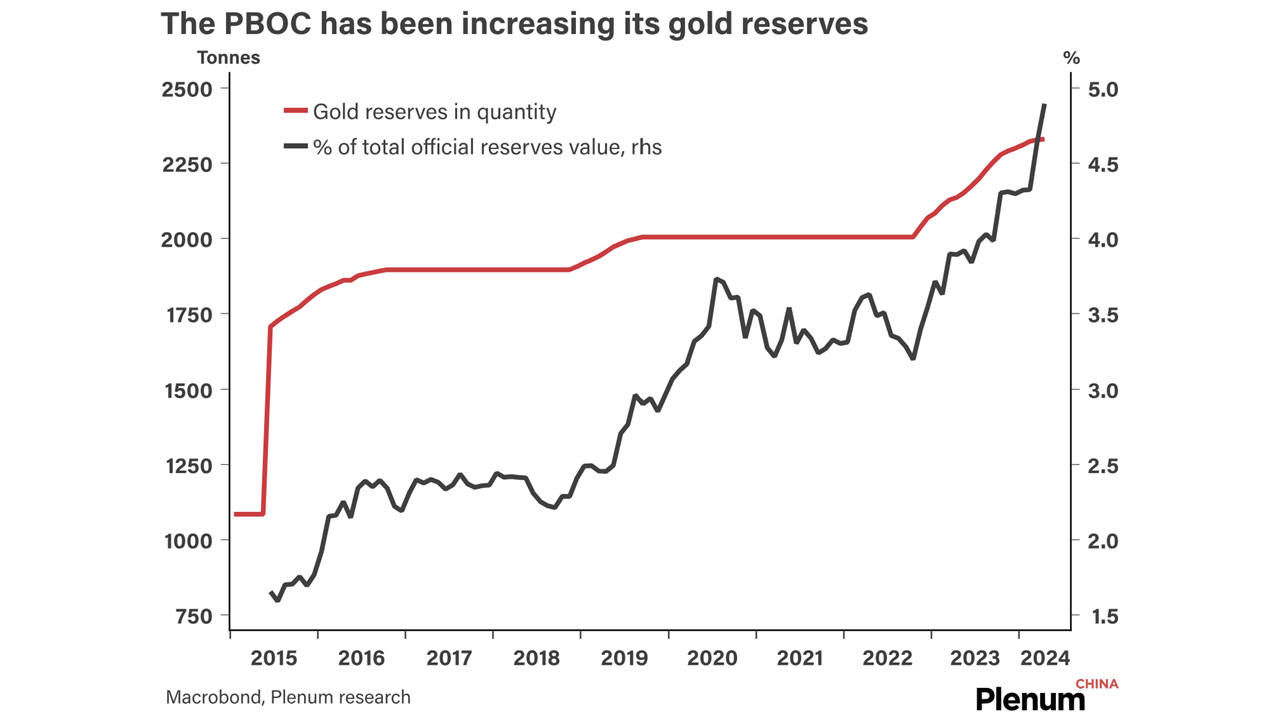

The PBOC’s declared gold reserves have been growing, but not by a large enough margin to explain the size of gold demand in China.