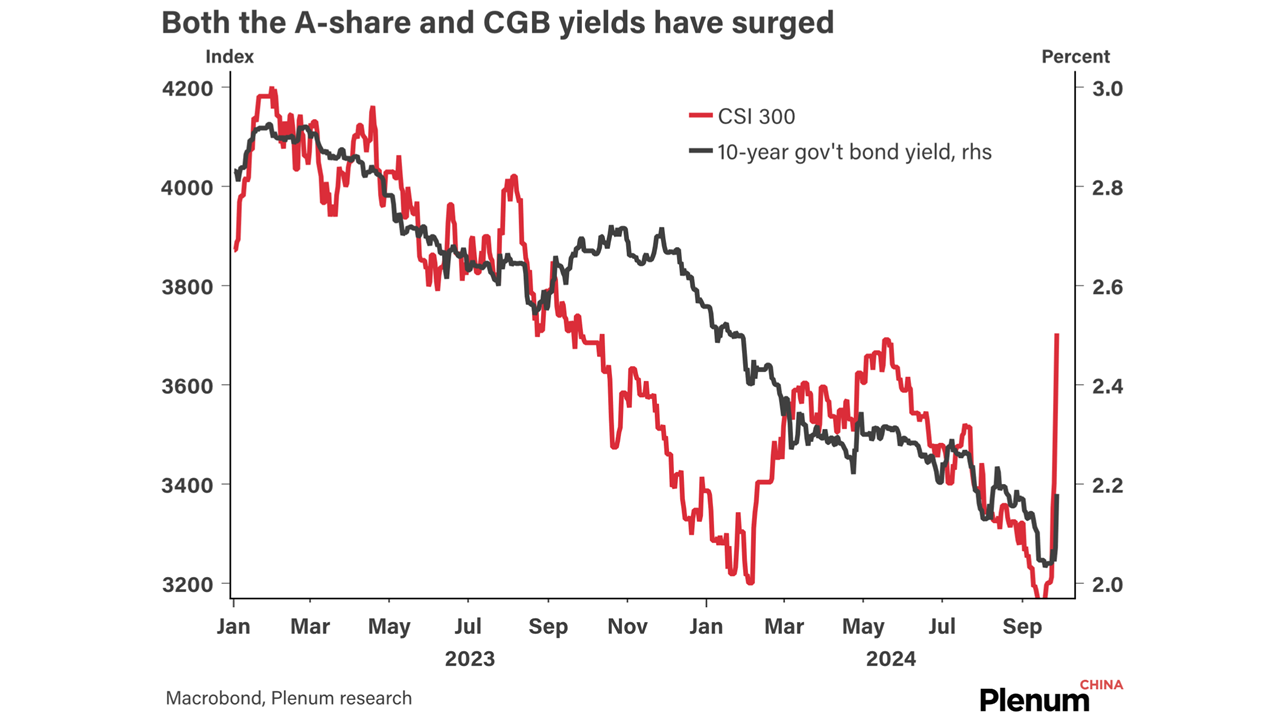

The A-share market rose further today after offshore equities recorded large gains during the holiday, but both have already faded from their peaks.

The A-share market rose further today after offshore equities recorded large gains during the holiday, but both have already faded from their peaks.

The Chinese stock market has had its strongest weekly rally since 2008 as investors have scrambled to buy and liquidity has poured in.

The PBOC cut policy rates by another 20bps, further loosened rules on the housing market, and created tools to help non-bank institutions buy stocks.

Robotaxi services captured the Chinese public’s imagination this summer as they reached a tipping point of visibility in cities like Wuhan.

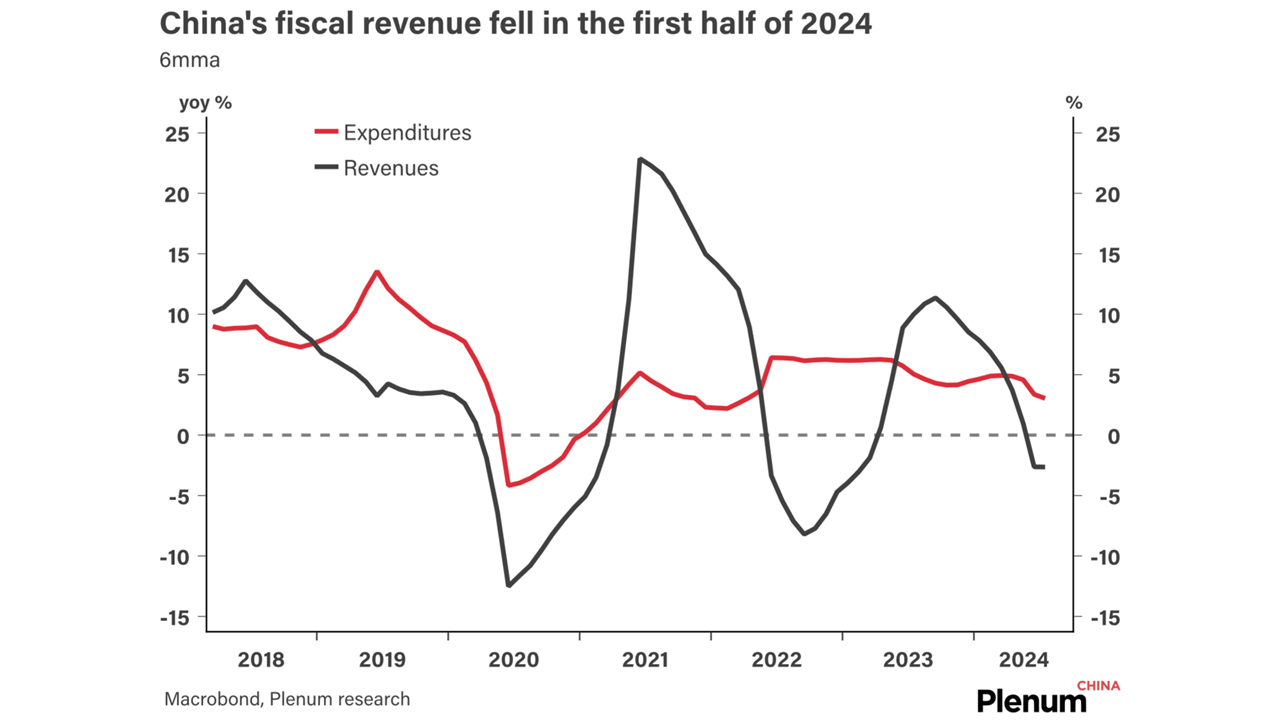

China’s fiscal revenue has fallen this year, painting a much worse picture than the headline GDP figure shows.

The latest thrust of the anti-corruption campaign in the financial sector is targeting executives at brokerages and mutual funds.

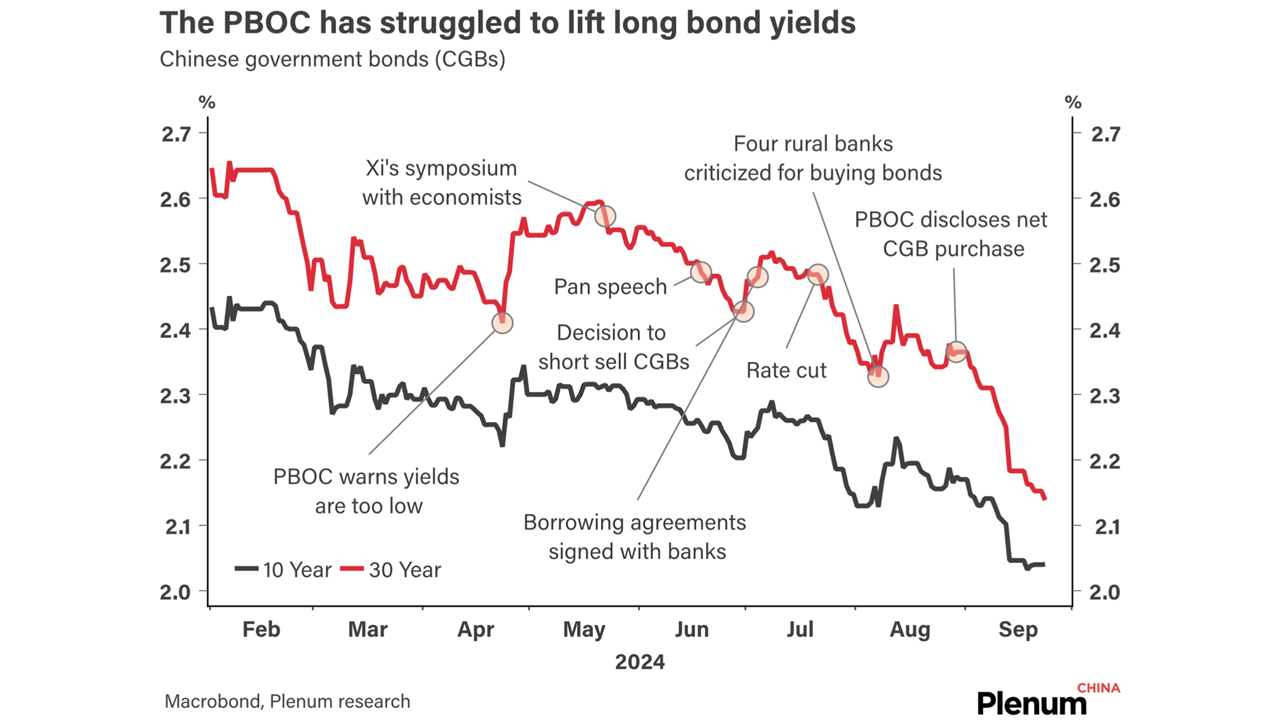

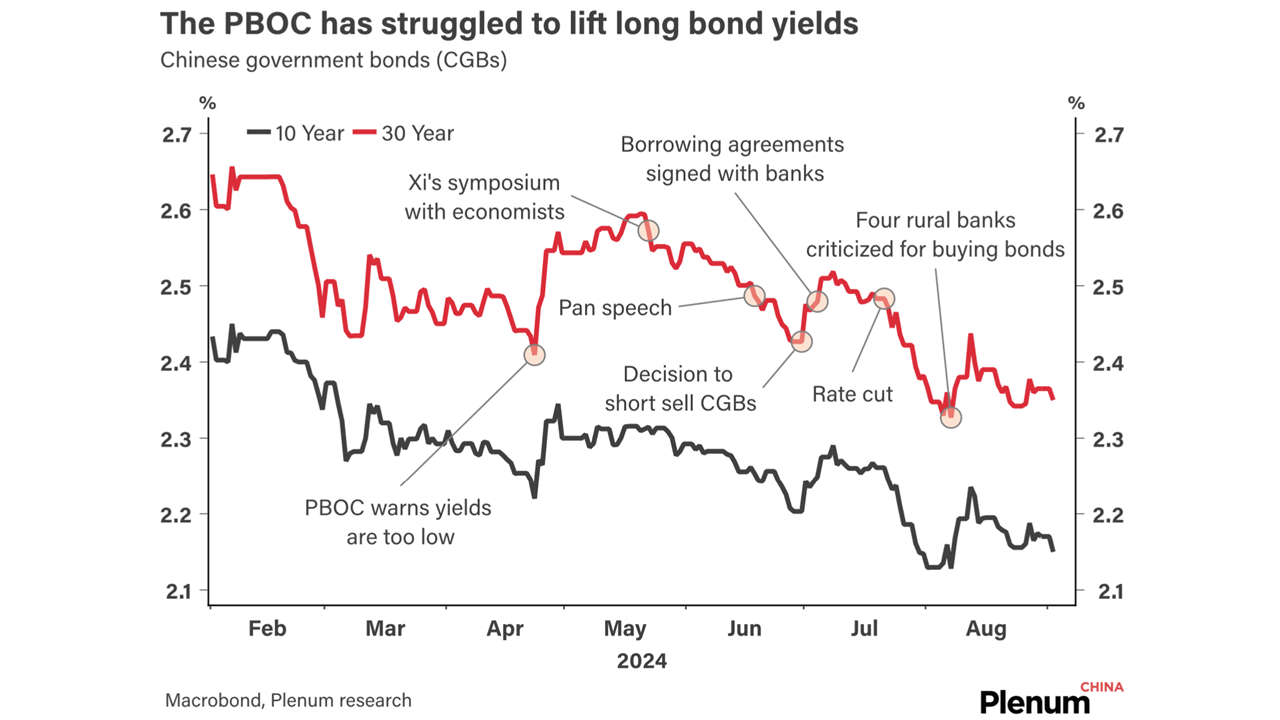

The PBOC net purchased RMB 100bn in government bonds after buying short-term bonds and selling long-term bonds in August.

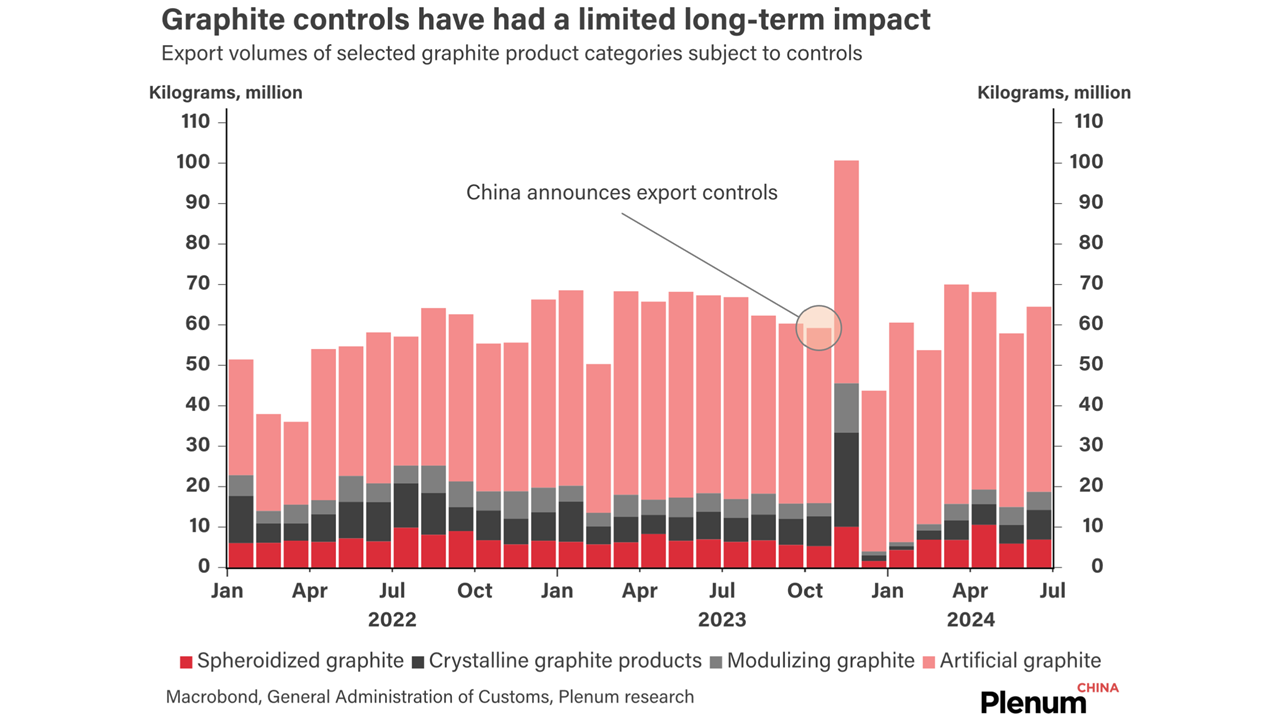

China is targeting critical minerals in which it has a comparative advantage over the West, but the controls have affected various products to different degrees.

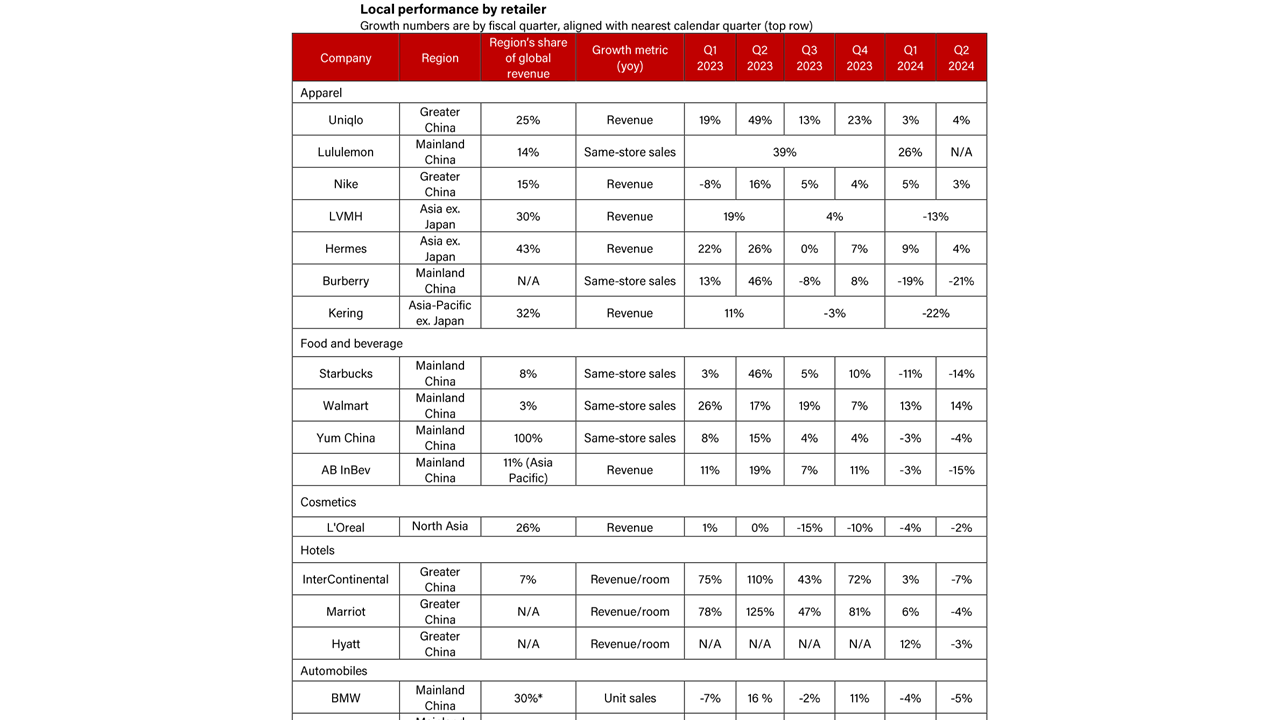

International retailers in China have been battered in 2024, with revenue falling broadly across many segments.

Recent market reforms have made some progress but fail to address the most fundamental problems facing Chinese equities.